When dealing with manufactured and mobile home financing, understanding the 21st mortgage repos process is crucial for both current borrowers and potential buyers. As the largest manufactured and mobile home lender in the United States, 21st Mortgage Corporation handles a significant number of repossessions annually, creating both challenges for borrowers and opportunities for buyers seeking affordable housing options.

What Are 21st Mortgage Repos?

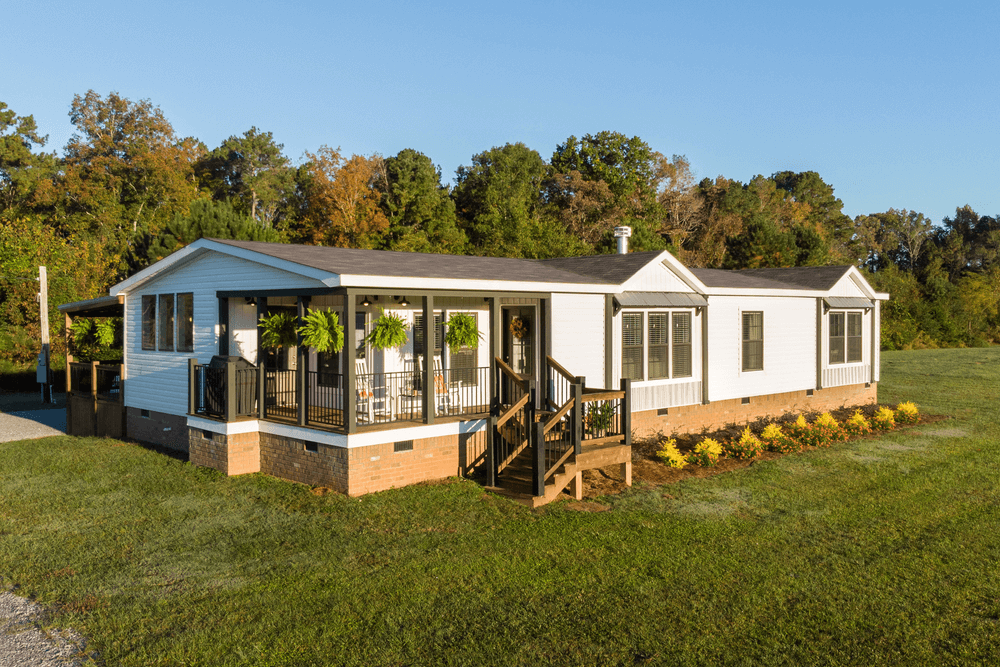

21st mortgage repos refer to manufactured and mobile homes that have been repossessed by 21st Mortgage Corporation due to borrower default. These properties are typically resold at significantly reduced prices, often 20-40% below market value, making them attractive options for budget-conscious homebuyers.

The repossession process occurs when borrowers fail to meet their mortgage obligations, leading 21st Mortgage to reclaim the property to recover their investment. These repossessed homes are then made available for sale through various channels, including the company’s official website and authorized dealers.

The 21st Mortgage Repossession Process

Initial Default and Notice Period

The 21st mortgage repos process begins when a borrower defaults on their loan payments. The specific timeline and procedures vary by state, but generally follow these steps:

Notice of Default (NOD): In states like California, 21st Mortgage can only issue a Notice of Default after the borrower has been in default for 90 days. This notice includes essential information such as the property address, borrower names, trustees, and lenders. It also provides details about the defaulted period, the deadline for loan repayment, and options available to halt the repossession process.

Notice of Trustee Sale (NTS): Following the NOD, most states require the issuance of a Notice of Trustee Sale to inform the public that a property owner has defaulted on their mortgage. This notice is typically published in local newspapers and posted on the property, providing transparency in the foreclosure process.

Pre-Foreclosure Options

Before proceeding with full repossession, 21st Mortgage often works with borrowers to explore alternatives. These may include loan modifications, payment plans, or other workout arrangements. However, if these efforts fail, the company will proceed with the formal foreclosure process.

Foreclosure and Repossession

Once all legal requirements are met and notice periods have expired, 21st Mortgage can proceed with repossessing the manufactured home. The specific process depends on whether the home is considered real property (permanently affixed to land) or personal property (chattel).

For homes classified as personal property, the repossession process is typically faster and follows procedures similar to vehicle repossessions. For homes considered real property, the process must follow state foreclosure laws, which can be more time-consuming and complex.

Finding 21st Mortgage Repos for Sale

Official 21st Mortgage Channels

The most reliable source for 21st mortgage repos is through the company’s official website and authorized dealers. 21st Mortgage maintains a directory of used and repossessed mobile and manufactured homes available for sale. These listings are regularly updated and provide detailed information about available properties.

Authorized Dealers and Retailers

21st Mortgage works with a network of authorized dealers who handle the sale of repossessed properties. These dealers have access to the company’s inventory and can help buyers navigate the purchase process, including financing options for qualified buyers.

Auction Sales

Some 21st mortgage repos are sold through public auctions, either online or at physical locations. These auctions can offer competitive pricing but require buyers to act quickly and often require cash purchases or pre-approved financing.

Benefits of Purchasing 21st Mortgage Repos

Significant Cost Savings

The primary advantage of purchasing repossessed homes is the substantial cost savings. Repo homes are typically priced 20-40% below market value, making homeownership more accessible for budget-conscious buyers.

Quality Assurance

Despite being repossessed, many of these homes are in good condition. 21st Mortgage and its dealers often perform necessary repairs and inspections before putting homes up for sale, ensuring buyers receive properties in livable condition.

Financing Opportunities

Buyers of 21st mortgage repos can often obtain financing through 21st Mortgage or other lenders, making these properties accessible even to those who cannot pay cash upfront.

Risks and Considerations

Limited Inspection Opportunities

Repossessed homes are typically sold “as-is,” meaning buyers have limited opportunities to inspect the property thoroughly before purchase. This can lead to unexpected repair costs after closing.

Competition from Other Buyers

Due to their attractive pricing, 21st mortgage repos often attract multiple buyers, creating competitive situations that may drive up the final sale price.

Legal and Title Issues

Buyers should ensure clear title transfer and verify that all liens and encumbrances are properly resolved before completing the purchase.

Tips for Successfully Purchasing 21st Mortgage Repos

Research and Preparation

Before shopping for repossessed homes, buyers should research the local market, understand current property values, and get pre-approved for financing. This preparation helps buyers act quickly when attractive properties become available.

Professional Inspection

Despite limitations, buyers should arrange for professional inspections whenever possible. This can help identify potential issues and provide bargaining power in negotiations.

Budget for Repairs

Even well-maintained repo homes may require some repairs or updates. Buyers should budget for these expenses and factor them into their overall purchase decision.

Work with Experienced Professionals

Partnering with real estate agents, attorneys, and lenders experienced in repo sales can help navigate the unique challenges and opportunities these transactions present.

The Future of 21st Mortgage Repos

As the manufactured housing market continues to evolve, 21st Mortgage repos remain an important segment of the affordable housing market. Economic factors, lending practices, and housing demand all influence the availability and pricing of these properties.

For buyers seeking affordable housing options, 21st mortgage repos represent a viable path to homeownership. However, success requires careful research, preparation, and understanding of the unique aspects of purchasing repossessed properties.

The key to successfully navigating the 21st mortgage repos market lies in understanding the process, knowing where to look for opportunities, and being prepared to act quickly when the right property becomes available. With proper preparation and realistic expectations, buyers can find quality manufactured homes at significantly reduced prices through the repo market.

(FAQs) About 21st Mortgage Repos

Q1 How much can I save by purchasing a 21st mortgage repo?

Buyers can typically save 20-40% below market value when purchasing repossessed homes from 21st Mortgage. The exact savings depend on the property’s condition, location, and current market conditions.

Q2 Can I get financing for a 21st mortgage repo?

Yes, financing is often available for repo purchases. 21st Mortgage and other lenders offer financing options for qualified buyers, though terms may vary from traditional home loans.

Q3 What is the condition of 21st mortgage repos?

Repo homes are sold “as-is,” but many are in good condition. 21st Mortgage and its dealers often perform basic repairs and maintenance before listing properties for sale.

Q4 How long does the 21st mortgage repossession process take?

The timeline varies by state and specific circumstances, but typically ranges from 90 days to several months. States like California require a minimum 90-day default period before starting the foreclosure process.

Q5Where can I find 21st mortgage repos for sale?

The best sources are 21st Mortgage’s official website, authorized dealers, and public auctions. The company maintains a directory of available used and repossessed homes that is regularly updated.

{kind=link}